Managing personal finances is a crucial aspect of achieving financial stability and reaching your long-term goals. One of the foundational tools for effective financial management is a personal budget. A budget helps you track your income, expenses, and savings, providing a clear roadmap for your financial journey.

Creating a personal budget may seem daunting at first, but with a systematic approach and commitment, you can gain control over your finances and make informed decisions about your money. Whether you’re aiming to pay off debt, save for a big purchase, or plan for retirement, a well-designed budget is essential.

In this step-by-step guide, we’ll walk you through the process of creating a personalized budget tailored to your financial goals and lifestyle. From identifying your income sources to categorizing expenses and setting realistic targets, each step will empower you to take charge of your finances and build a solid foundation for financial success.

Let’s embark on this journey towards financial empowerment, starting with the first step: assessing your income and expenses.

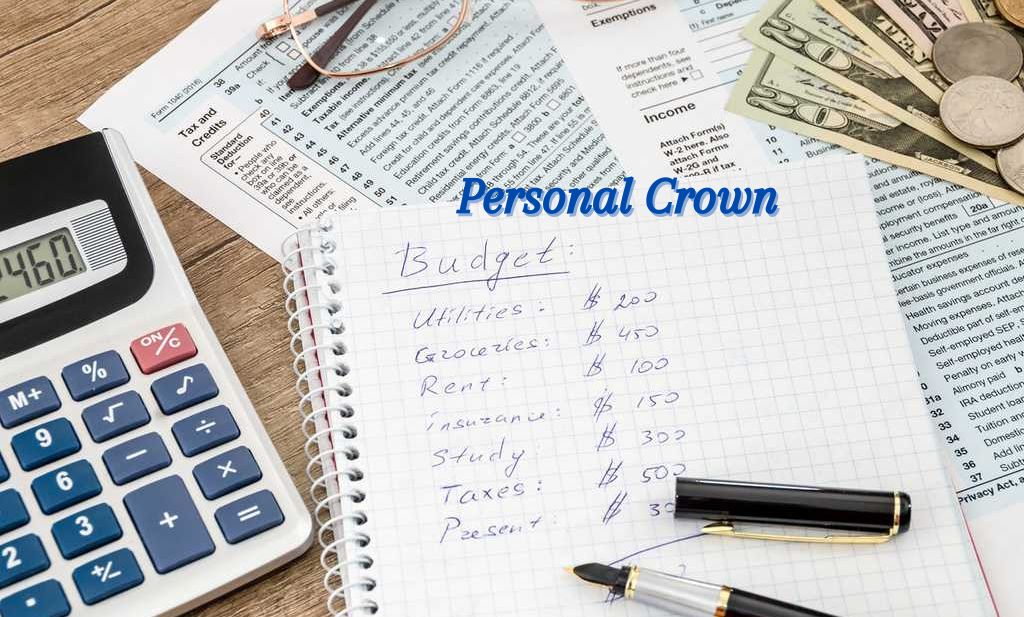

What is a Budget?

A budget is a monetarist plan that outlines your expected income and expenses over an explicit period, typically on a monthly base. It serves as a roadmap for managing your money by allocating funds to different categories such as housing, transportation, groceries, savings, and entertainment. A well-crafted budget helps you prioritize your spending, identify areas where you can save, and work towards achieving your financial goals. It provides a clear picture of your financial health, allowing you to make informed decisions about how to use your resources effectively. Ultimately, a budget is a powerful tool for taking control of your finances and working towards a more secure financial future.

How to Make a Budget in 5 Steps

Creating a budget can seem overwhelming, but breaking it down into manageable steps can simplify the process. Here’s a straightforward guide to making a budget in five steps:

- Assess Your Income:

Start by calculating your total monthly income from all sources, including salaries, wages, bonuses, freelance work, and any other sources of revenue. This step provides a clear understanding of how much money you have available to allocate towards expenses and savings.

- Track Your Expenses:

Record all your expenses over the course of a month to understand where your money is going. Categorize expenses into fixed costs (such as rent, utilities, and loan payments) and variable costs (like groceries, dining out, and entertainment). Tracking expenses helps identify spending patterns and areas where you can cut back or optimize.

- Set Financial Goals:

Determine your short-term and long-term financial goals, whether it’s paying off debt, saving for a vacation, buying a house, or building an emergency fund. Setting specific, measurable, achievable, relevant, and time-bound (SMART) goals provides clarity and motivation for budgeting effectively.

- Create a Budget Plan:

Based on your income, expenses, and financial goals, create a budget plan that allocates funds to different expense categories. Aim to prioritize essential expenses while also allocating funds towards savings and discretionary spending. Ensure that your budget is realistic and flexible enough to accommodate unexpected expenses or changes in income.

- Monitor and Adjust:

Regularly review your budget to track your progress and make adjustments as needed. Compare your actual spending against your budgeted amounts to identify any discrepancies and adjust your plan accordingly. Flexibility is key to successful budgeting, so be prepared to tweak your budget as your financial situation evolves.

By following these five steps, you can create a personalized budget that empowers you to take control of your finances, achieve your financial goals, and build a secure financial future.

Money management

Money management refers to the process of overseeing and controlling your financial resources effectively. It involves making informed decisions about how to earn, spend, save, invest, and budget your money to achieve your financial goals and maximize your overall financial well-being.

Effective money management requires careful planning, discipline, and financial literacy. It encompasses various aspects, including:

- Budgeting:

Making a budget to track income and costs, prioritize spending, and apportion funds towards savings and financial goals.

- Saving:

Setting aside a portion of your income regularly for emergencies, future expenses, and long-term goals such as retirement or education.

- Investing:

Making strategic decisions about how to grow your wealth by investing in assets such as stocks, bonds, real estate, or retirement accounts.

- Debt Management:

Managing debt responsibly by making timely payments, reducing high-interest debt, and developing a plan to pay off outstanding balances

- Financial Planning:

Developing a comprehensive plan to achieve your short-term and long-term financial goals, such as buying a house, starting a business, or saving for children’s education.

- Risk Management:

Protecting your financial security by obtaining insurance coverage for health, life, disability, and property.

- Tracking and Monitoring:

Regularly monitoring your financial situation, reviewing your budget, tracking spending habits, and adjusting your financial plan as needed.

By practicing sound money management principles, individuals can build financial stability, minimize financial stress, and work towards achieving their financial aspirations. Additionally, effective money management skills are essential for navigating life’s financial challenges and opportunities with confidence and resilience.

Financial planning

Financial planning is the process of setting goals, assessing resources, and creating a roadmap to achieve desired financial outcomes. It involves studying your current financial condition, identifying your financial goals, and emerging policies to meet those goals within a specified timeframe. Financial planning encompasses various aspects of personal finance, including budgeting, saving, investing, risk management, retirement planning, and estate planning.

Key components of financial planning include:

- Goal Setting:

Clearly defining short-term and long-term financial goals, such as buying a home, saving for education, retiring comfortably, or leaving a legacy for future generations.

2. Financial Assessment:

Evaluating your current financial situation by analyzing income, expenses, assets, liabilities, cash flow, and net worth.

3. Risk Management:

Identifying potential risks that could impact your financial stability, such as job loss, disability, illness, or unexpected expenses, and implementing strategies to mitigate these risks through insurance and emergency funds.

- Budgeting:

Creating a budget to track income and expenses, allocate funds towards essential needs, savings, and discretionary spending, and ensure that spending aligns with your financial goals.

- Saving and Investing:

Developing a systematic approach to saving money and investing in diversified assets to grow wealth over time and achieve long-term financial objectives.

- Retirement Planning:

Estimating future retirement expenses, determining retirement income needs, and creating a plan to build retirement savings through employer-sponsored plans like 401(k)s, individual retirement accounts (IRAs), and other investment vehicles.

- Tax Planning:

Strategizing to minimize tax liabilities through tax-efficient investing, retirement contributions, deductions, credits, and other tax planning strategies.

- Estate Planning:

Organizing your affairs to ensure the orderly transfer of assets to beneficiaries, minimize estate taxes, and specify your wishes regarding healthcare decisions, guardianship of minors, and asset distribution after death.

By engaging in comprehensive financial planning, individuals can gain clarity about their financial goals, make informed decisions, and take proactive steps to secure their financial future and achieve greater peace of mind. Additionally, working with a qualified financial advisor can provide valuable expertise and guidance to navigate complex financial matters and optimize your financial plan for success.

Conclusion

In conclusion, creating a personal budget is a fundamental step towards gaining control over your finances and achieving your financial goals. By following the step-by-step guide outlined above, you can assess your income, track your expenses, set realistic financial goals, create a budget plan, and monitor your progress. A well-designed budget empowers you to prioritize spending, identify areas for savings, and make informed decisions about your money. With dedication and discipline, you can use your budget as a powerful tool to build financial stability, reduce financial stress, and work towards a secure financial future. Start your journey towards financial empowerment today by taking control of your finances through effective budgeting.

FAQ (Frequently Asked Question)

What is the personal budget?

An individual financial plan is a money plan which designates future pay towards costs, investment funds and obligation reimbursement. Individual planning requires both making a feasible arrangement and following it.

How do you write your own budget?

How to make a budget plan

Compute your month to month pay. Computing the amount, you procure every month or year is a basic early move toward making a financial arrangement. …

Track your ways of managing money. …

Put forth objectives for your cash. …

Make an arrangement. …

Make changes as the need might arise. …

Set a timetable for checking in with your arrangement.