In today’s unpredictable world, where unexpected expenses can arise at any moment, having a robust emergency fund is essential for securing your financial future. Whether it’s a sudden medical bill, car repairs, or unexpected job loss, having a safety net in place can provide peace of mind and stability during times of uncertainty. Building an emergency fund isn’t just about being prepared for the worst-case scenarios; it’s about empowering yourself to navigate life’s challenges with confidence and resilience. In this guide, we’ll explore the essentials of building and maintaining an emergency fund, helping you establish a solid foundation for your financial security.

Understanding the Importance of an Emergency Fund

An emergency fund serves as a financial buffer against life’s unforeseen events, providing a sense of stability and security in times of crisis. Whether faced with sudden medical expenses, unexpected home repairs, or a sudden loss of income, having readily accessible funds can help mitigate the stress and impact of such situations. Without an emergency fund, individuals may find themselves forced to rely on high-interest loans, credit cards, or even dipping into retirement savings, exacerbating financial strain in the long term. By understanding the importance of an emergency fund and proactively building one, individuals can safeguard their financial well-being and better navigate the uncertainties of life.

How Much Should You Save in Your Emergency Fund?

Determining the appropriate amount to save in your emergency fund depends on various factors such as your monthly expenses, income stability, and individual circumstances. However, a common recommendation is to save enough to cover at least three to six months’ worth of living expenses. This cushion can provide financial security during unexpected events like job loss, medical emergencies, or major car repairs, ensuring you have a safety net to fall back on without resorting to high-interest debt or depleting other savings accounts. Adjustments may be necessary based on your specific situation, but aiming for this range can offer peace of mind and stability in times of crisis.

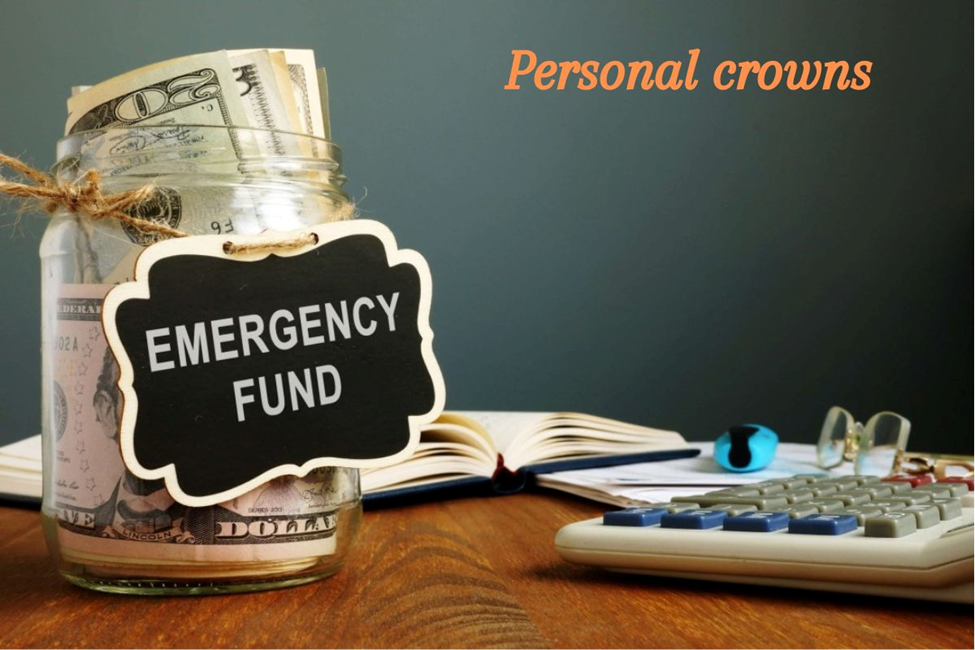

Emergency Fund Essentials

An emergency fund is a critical section of financial solidity. It acts as a safety net, providing a financial cushion to cover unexpected expenses or periods of income loss. Here are some essentials for building and maintaining an emergency fund:

1. Set a Goal:

Determine how widely you want to save in your emergency trust. A common recommendation is to aim for 3 to 6 months’ worth of living expenses, but this can vary based on individual circumstances such as job stability, family size, and expenses.

2. Create a Budget:

Track your income and expenses to understand your cash flow. Distribute a portion of your income definitely for building your emergency fund. Cut unnecessary expenses to free up more money for savings.

3. Choose a Separate Account:

Keep your emergency fund discrete from your regular inspection or funds accounts. Consider a high-yield savings account or a money market account that offers easy access to funds while still earning some interest.

4. Automate Savings:

Set up automatic transfers from your paycheck or checking account to your emergency fund account. This ensures consistent contributions and removes the temptation to spend the money elsewhere.

5. Start Small, Build Over Time:

If you can’t save the full recommended amount immediately, start with a smaller goal and gradually increase it as your financial situation improves.

6. Review and Adjust Regularly:

Periodically review your emergency fund to ensure it aligns with your current financial situation and goals. Adjust your savings contributions, if necessary, especially after major life changes like a job loss or increase in expenses.

7. Use Only for Emergencies:

Reserve your emergency fund for true emergencies, such as unexpected medical expenses, car repairs, or job loss. Avoid dipping into it for non-essential purchases or vacations.

8. Replenish After Use:

If you do need to use your emergency fund, prioritize replenishing it as soon as possible to maintain your financial safety net.

9. Consider Insurance Coverage:

Certain types of insurance, such as health insurance, disability insurance, and homeowners or renters’ insurance, can provide additional protection against unexpected expenses. Review your coverage regularly to ensure it meets your needs.

10. Stay Flexible:

Life is unpredictable, so be prepared to adjust your emergency fund strategy as needed. Be proactive in managing your finances and building resilience against unexpected challenges.

Savings cushion

A savings cushion refers to a financial reserve set aside to handle unexpected expenses or financial emergencies. It serves as a protective buffer, providing stability and peace of mind in times of need. Here are some key aspects of a savings cushion:

· Purpose:

The primary purpose of a savings cushion is to cover unforeseen expenses that could disrupt your financial stability, such as medical emergencies, car repairs, or sudden job loss.

· Size:

The size of your savings cushion depends on your individual circumstances, including your income, expenses, and financial obligations. A common recommendation is to aim for 3 to 6 months’ worth of living expenses, but this can vary based on factors like job security, family size, and lifestyle.

· Accessibility:

Your savings cushion should be readily accessible in case of emergencies. Consider keeping it in a separate savings account that offers easy withdrawal options, such as a high-yield savings account or a money market account.

· Regular Contributions:

Building a savings cushion requires consistent contributions over time. Allocate a portion of your income specifically for this purpose and set up automatic transfers to ensure regular deposits into your savings account.

· Emergency Fund vs. Savings Cushion:

While the terms are often used interchangeably, some people distinguish between an emergency fund, which covers immediate expenses like medical bills or car repairs, and a savings cushion, which is a broader reserve for any unexpected financial needs.

· Review and Adjust:

Periodically review your savings cushion to ensure it remains adequate for your current financial situation and needs. Adjust your savings goals and contributions as necessary, especially after major life changes like a job change or significant expenses.

· Purposeful Spending:

Avoid tapping into your savings cushion for non-essential purchases or discretionary spending. Reserve it solely for genuine emergencies to maintain its effectiveness as a financial safety net.

· Replenishment:

If you need to use funds from your savings cushion, prioritize replenishing them as soon as possible to restore your financial security. Make it a priority to rebuild your cushion to its target size.

· Insurance Coverage:

While a savings cushion provides important financial protection, certain types of insurance, such as health insurance, disability insurance, and homeowners or renters insurance, can offer additional protection against specific risks. Review your insurance coverage regularly to ensure it adequately protects you and your assets.

· Financial Peace of Mind:

A robust savings cushion not only provides financial security but also offers peace of mind, knowing that you’re prepared to handle unexpected challenges and emergencies that may arise.

Financial safety net

A financial safety net refers to a collection of resources and strategies that individuals or households put in place to protect themselves from unexpected financial hardships or emergencies. It serves as a cushion to mitigate the impact of unforeseen events and maintain financial stability. Here are the key components of a financial safety net:

1. Emergency Fund:

An extra fund is a dedicated savings account definitely kept to cover unforeseen costs such as medical emergencies, car repairs, or sudden job loss. It provides immediate access to funds when needed most.

2. Insurance Coverage:

Insurance policies, such as health insurance, life insurance, disability insurance, and homeowners or renters’ insurance, play a critical role in safeguarding against specific risks. These policies help cover expenses related to health care, loss of income, property damage, and liability, reducing the financial burden during difficult times.

3. Debt Management:

Maintaining manageable levels of debt and having a plan in place to pay off outstanding balances can help prevent financial crises. Strategies such as budgeting, prioritizing high-interest debt, and negotiating repayment terms can contribute to long-term financial stability.

4. Diverse Income Sources:

Relying on a single source of income leaves individuals vulnerable to income disruptions. Diversifying income streams through side hustles, freelance work, investments, or passive income sources can provide additional financial security.

5. Job Skills and Training:

Continuously updating and enhancing job skills through education, training programs, or certifications can improve employability and resilience in the face of economic uncertainty. Acquiring transferable skills and staying adaptable to changes in the job market are essential for maintaining financial security.

6. Support Networks:

Building a support network of family, friends, or community resources can provide emotional and financial assistance during challenging times. Having a trusted circle of individuals to turn to for advice, temporary housing, or financial assistance can help weather unexpected storms.

7. Financial Planning and Budgeting:

Developing a comprehensive financial plan and adhering to a budget can help individuals prioritize saving, manage expenses, and allocate resources effectively. Regularly reviewing and adjusting financial goals and spending habits ensures that the safety net remains robust and adaptable to changing circumstances.

8. Long-Term Savings and Investments:

Investing in retirement accounts, such as 401(k)s or IRAs, and other long-term investment vehicles provides a source of income and financial security in the future. Building wealth through prudent investment strategies contributes to overall financial resilience.

9. Contingency Planning:

Anticipating potential risks and developing contingency plans for various scenarios, such as job loss, natural disasters, or unexpected expenses, helps individuals prepare for emergencies proactively. Having a plan in place reduces the impact of unforeseen events and facilitates a quicker recovery.

10. Regular Review and Maintenance:

Periodically assessing the effectiveness of the financial safety net and making adjustments as needed ensures its continued relevance and adequacy. Life circumstances change, so regularly revisiting and updating financial goals, insurance coverage, and emergency preparedness measures is essential for maintaining financial security.

Rainy day fund

A rainy-day fund is like a financial umbrella for unexpected storms. It’s a stash of money set aside specifically for unforeseen expenses or emergencies that can suddenly pour down on your finances, such as car repairs, medical bills, or unexpected job loss. This fund acts as a buffer, providing peace of mind and stability when life throws a curveball. By regularly contributing to your rainy-day fund and keeping it separate from your everyday expenses, you ensure that you’re prepared to weather any financial downpour that comes your way.

Conclusion

In conclusion, establishing and maintaining an emergency fund is a cornerstone of building financial security for the future. By diligently following the essentials outlined setting a goal, creating a budget, choosing a separate account, automating savings, starting small and building over time, reviewing and adjusting regularly, using funds only for emergencies, replenishing after use, considering insurance coverage, and staying flexible individuals can cultivate a strong financial safety net. With a well-prepared emergency fund in place, individuals gain confidence in their ability to withstand unexpected financial challenges, ensuring greater stability and peace of mind for the future. By prioritizing financial preparedness today, individuals pave the way for a more secure and resilient tomorrow.

FAQ (Frequently Asked Question)

How do I secure my emergency fund?

Moves toward Construct a Just-in-case account.

Put forth a few more modest reserve funds objectives, instead of one enormous one. Put yourself in a good position all along. …

Begin with little, normal commitments. …

Mechanize your reserve funds. …

Try not to increment month to month spending or open new charge cards. …

Try not to over-save.

Why should you save an emergency fund?

Crisis assets can assist with paying in case of surprising clinical and dental bills, home and auto fixes, and employment misfortunes, however they can likewise take care of other unexpected expenses. For example, late years have seen increasing costs on everything from food to ga